5 Stages Of M&A Transaction: What Every Business Should Know

Transactions involving mergers and acquisitions (M&A) are never the same. More complex stages of m&a transactions typically have different structures based on a variety of factors, including the size of the transaction, any international components, potential employees of the target company, competition issues, regulatory consequences, financial considerations, and the parties’ relationship.

Having said that, an M&A transaction typically follows the procedure described in more detail below, whether it involves buying stock in the target company or the target entity’s operations. Naturally, this particular procedure is not rigid and may change based on how complicated the transaction in question is. Indeed, several of the steps listed below may be skipped entirely or shortened in a more easy M&A transaction.

Stages of M&A Transaction

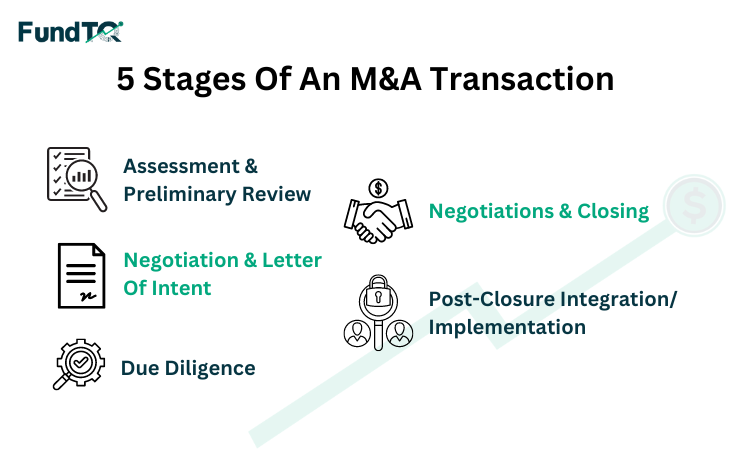

Here are 5 stages of m&a transaction:

1. Assessment And Preliminary Review

In the event that a buyer cannot be located, an information memorandum is typically used to start the M&A transaction process. Typically, the vendor drafts the information memo and publishes it with the intention of determining market interest and, in the end, selling the firm or a portion of it for the highest possible price.

Without disclosing any sensitive or confidential business information about the target, an information memorandum typically provides the prospective buyer with enough details to decide whether to pursue the acquisition of the target company or business.

A prospective buyer, or buyers if there were more than one, would normally engage in a Non-Disclosure Agreement (NDA), which is meant to preserve the target company’s confidentiality and the sensitive data relevant to its business.

2. Negotiation And Letter Of Intent

The due diligence process, which is described below, typically comes before this second step when multiple possible buyers are involved. But, in the event that there is just one buyer in the running, it is customary for the parties to begin deliberating over some issues prior to the sale’s contractual phase, either before or at the same time as the due diligence process begins. These issues consist of the following:

- competition/antitrust law implications, and whether such transaction necessitates pre-clearance from the Office for Competition;

- employment law considerations;

- licensing matters; and

- fiscal implications, amongst others.

Additionally, it is typical for the vendor and possible buyer to lay out the terms and conditions of the proposed acquisition in a letter of intent, which is typically not legally enforceable.

3. Due Diligence

Doing a due diligence examination on the target company or business at this time is a typical procedure. Buyer due diligence occurs when there is only one potential buyer, and advisors engaged by the buyer usually carry out the due diligence procedure.

A vendor may also decide to carry out a due diligence exercise for a number of reasons. Basically, a vendor’s due diligence can either help to close a deal (in which case the buyer could choose to rely on it and protect its position with warranties and benefits) or identify any possible problems that might slow down the deal, influence the terms of the sale, or have an effect on the warranties the seller can offer to the buyer.

Due diligence covers legal and financial aspects, but its main goals are to find the biggest risks involved in a proposed purchase, set reasonable prices, and fortify one’s position during talks. The due diligence process itself may cover a range of legal topics from a legal perspective in order to fully investigate the target or its operations. These topics may include corporate matters, contractual and commercial obligations, employment, data protection, intellectual property, insurance, and regulatory and compliance matters.

4. Negotiations And Closing

Following the completion of the due diligence process, the buyer-to-be would usually review the results with its advisors to determine how significant they are to the deal. If the purchaser remains interested in proceeding with the acquisition, the parties typically negotiate the transaction details, including all terms and conditions. Depending on whether the transaction involves purchasing shares or the business, they may also negotiate the final price or agree on a mechanism to determine the sale price. Additionally, they settle the specifics of warranties, indemnities, and any limitations included in a Share Purchase Agreement (SPA) or an Assets Purchase Agreement (APA).

5. Post-Closure Integration/Implementation

It’s typical for the SPA/APA to include clauses that kick in after the closing, like extra obligations the parties must meet, finishing up the transfer of extra assets, obtaining approvals, notifying parties, putting in place a price adjustment mechanism, or signing other relevant contracts.

In addition to executing these post-closing activities, the parties can think about going through a post-closing integration exercise to merge the two businesses or enterprises and maximize synergies to guarantee the deal’s success.