Top 100 Indian Startups in 2026

India is home to some of the world’s fastest-growing startup companies. From fintech and SaaS to healthcare, ecommerce, AI, and consumer brands, Indian startups are creating billion-dollar businesses and transforming industries. This guide covers the top Indian startups in 2026, including their founders, funding raised, business models, valuations, and the key lessons entrepreneurs can learn from their growth journeys.

Whether you are an investor, founder, student, or startup enthusiast, this list provides a comprehensive overview of India’s most successful startup companies.

.

Quick Answer: Which Are the Top Indian Startups in 2026?

Quick Answer: Which Are the Top Indian Startups in 2026?

Some of the top startups in India include CRED, Groww, Razorpay, Zerodha, Zepto, Meesho, Nykaa, Dream11, Udaan, PharmEasy, Lenskart, and PhysicsWallah. These companies are among the most successful startups in India because they have achieved strong customer growth, significant funding, scalable business models, and leadership positions in their respective industries. India’s startup ecosystem now includes more than 100 unicorns across fintech, ecommerce, SaaS, healthtech, AI, logistics, and consumer technology sectors.

Top Startup Companies in India at a Glance

The table below highlights some of the most successful startups in India based on market presence, funding, innovation, and growth.

| Startup | Sector | Founder |

| Zerodha | Fintech | Nithin Kamath |

| Razorpay | Fintech | Harshil Mathur |

| CRED | Fintech | Kunal Shah |

| Groww | WealthTech | Lalit Keshre |

| PhonePe | Fintech | Sameer Nigam |

| Jupiter | Fintech | Jitendra Gupta |

| Slice | Fintech | Rajan Bajaj |

| Navi | Fintech | Sachin Bansal |

| Open | Fintech | Anish Achuthan |

| BharatPe | Fintech | Ashneer Grover |

| Nykaa | Beauty Commerce | Falguni Nayar |

| Meesho | Social Commerce | Vidit Aatrey |

| Zepto | Quick Commerce | Aadit Palicha |

| Lenskart | Eyewear Commerce | Peyush Bansal |

| FirstCry | Baby Products | Supam Maheshwari |

| Purplle | Beauty Commerce | Manish Taneja |

| boAt | Consumer Electronics | Aman Gupta |

| Blinkit | Quick Commerce | Albinder Dhindsa |

| Udaan | B2B Commerce | Sujeet Kumar |

| ElasticRun | Logistics | Saurabh Nigam |

| Freshworks | SaaS | Girish Mathrubootham |

| Zoho | SaaS | Sridhar Vembu |

| Chargebee | SaaS | Krish Subramanian |

| BrowserStack | SaaS | Ritesh Arora |

| Postman | SaaS | Abhinav Asthana |

| CleverTap | SaaS | Sunil Thomas |

| Uniphore | AI & SaaS | Umesh Sachdev |

| Yellow.ai | Conversational AI | Raghu Ravinutala |

| Sarvam AI | Artificial Intelligence | Vivek Raghavan |

| Krutrim | Artificial Intelligence | Bhavish Aggarwal |

| PharmEasy | HealthTech | Dharmil Sheth |

| Tata 1mg | HealthTech | Prashant Tandon |

| Practo | HealthTech | Shashank ND |

| MediBuddy | HealthTech | Satish Kannan |

| Niramai | HealthTech AI | Geetha Manjunath |

| Dream11 | SportsTech | Harsh Jain |

| MPL | Gaming | Sai Srinivas |

| PhysicsWallah | EdTech | Alakh Pandey |

| Unacademy | EdTech | Gaurav Munjal |

| Vedantu | EdTech | Vamsi Krishna |

| Ola | Mobility | Bhavish Aggarwal |

| Ather Energy | EV | Tarun Mehta |

| BluSmart | EV Mobility | Anmol Singh Jaggi |

| Skyroot Aerospace | SpaceTech | Pawan Kumar Chandana |

| Agnikul Cosmos | SpaceTech | Srinath Ravichandran |

| The Good Glamm Group | D2C | Darpan Sanghvi |

| Noise | Wearables | Gaurav Khatri |

| Wakefit | D2C Furniture | Ankit Garg |

| Country Delight | FoodTech | Chakradhar Gade |

| Rebel Foods | Cloud Kitchen | Jaydeep Barman |

Top 50 Indian Startups in 2026 by Sector

India’s startup ecosystem is one of the largest in the world, with companies operating across fintech, SaaS, ecommerce, healthcare, artificial intelligence, mobility, logistics, and consumer technology. The startups listed below are among the most influential and fastest-growing companies in India based on innovation, market adoption, funding activity, and long-term growth potential.

Fintech Startups

-

Razorpay

-

Zerodha

-

CRED

-

Groww

-

PhonePe

-

BharatPe

-

Jupiter

-

Slice

-

Navi

-

Open

SaaS & Enterprise Technology Startups

-

Zoho

-

Freshworks

-

Chargebee

-

BrowserStack

-

Postman

-

CleverTap

-

Whatfix

-

Kissflow

-

LeadSquared

-

Druva

Ecommerce & Consumer Startups

-

Nykaa

-

Meesho

-

Zepto

-

Lenskart

-

FirstCry

-

Purplle

-

boAt

-

Wakefit

-

The Good Glamm Group

-

Country Delight

Healthcare & HealthTech Startups

-

PharmEasy

-

Tata 1mg

-

Practo

-

MediBuddy

-

Niramai

-

HealthifyMe

-

Redcliffe Labs

AI & DeepTech Startups

-

Sarvam AI

-

Krutrim

-

Uniphore

-

Yellow.ai

-

Mad Street Den

-

Gnani.ai

EdTech Startups

-

PhysicsWallah

-

Unacademy

-

Vedantu

-

upGrad

-

Teachmint

Mobility, Logistics & SpaceTech Startups

-

Ola

-

Ather Energy

-

BluSmart

-

Udaan

-

ElasticRun

-

Skyroot Aerospace

-

Agnikul Cosmos

These startups represent some of the best startup companies in India and continue to attract attention from founders, investors, venture capital firms, and strategic acquirers. Their growth stories offer valuable lessons in fundraising, customer acquisition, product innovation, market expansion, and long-term business building.

Why Successful Indian Startups Are Built Differently

India’s startup ecosystem is being shaped by UPI-led digital infrastructure, affordable mobile internet, a young digital consumer base, and a deeper investor network across angels, family offices, venture capital, private equity, and strategic acquirers. As of 2026, India has more than 2 lakh DPIIT-recognised startups, making the ecosystem broader and more competitive than ever. The best Indian startups are no longer judged only by valuation or growth-at-any-cost metrics. Investors are now paying closer attention to revenue quality, contribution margins, customer retention, governance, compliance, and the ability to build a sustainable path to profitability.

Government initiatives such as Startup India have supported the ecosystem through recognition, tax benefits, easier compliance, and access to startup-focused schemes. But the larger driver is the rise of experienced operators, second-time founders, domain specialists, and finance-aware entrepreneurs who understand both execution and capital markets.

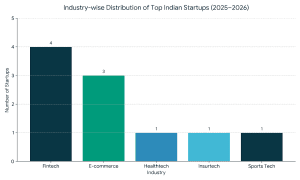

Snapshot: Top Indian Startups at a Glance in 2026

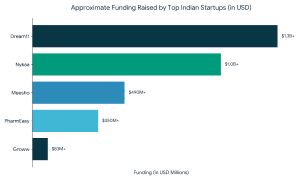

Approximate Funding Raised by Top Indian Startups (in USD)

What These Startups Have in Common — and What Founders Can Borrow

What These Startups Have in Common — and What Founders Can Borrow

What These Startups Have in Common — and What Founders Can Borrow

What These Startups Have in Common — and What Founders Can BorrowEach company below solved a real market gap, built trust at scale, and used capital as a strategic tool. The strongest patterns are clear: category focus, sharp customer insight, strong distribution, clean cap tables, sector-specific investors, and founders who treated fundraising as a structured process rather than a last-minute activity.

Building a Startup and Planning Your Next Fundraise?

Many of India’s fastest-growing startups prepared for fundraising long before approaching investors. Strong financial models, investor-ready pitch decks, clean cap tables, and a clear growth story often make the difference between a successful raise and months of wasted outreach.

Explore FundTQ’s Startup Fundraising Advisory, Valuation Support, and Pitch Deck Services to understand how investors evaluate growing companies.

Top 10 Startups in India

1. CRED

2. Groww

3. Zerodha

4. Razorpay

5. Zepto

6. Nykaa

7. Meesho

8. Udaan

9. Lenskart

10. Dream11

Most Successful Startups in India

The most successful startups in India are companies that have achieved large-scale adoption, sustainable revenue growth, and strong investor confidence. Examples include Zerodha, Nykaa, Groww, Razorpay, and CRED.

Startup Companies in Bangalore

Bangalore remains India’s startup capital. Leading startup companies in Bangalore include:

– Razorpay

– Groww

– CRED

– Zerodha

– Udaan

– PhonePe

– Slice

– Jupiter

Emerging Startups in India to Watch

Alongside established unicorns, several emerging startups are attracting attention from investors, customers, and strategic acquirers.

Some notable emerging Indian startups include:

-

Sarvam AI

-

Krutrim

-

Skyroot Aerospace

-

Agnikul Cosmos

-

BluSmart

-

Juspay

-

Niramai

-

The Good Glamm Group

These startups operate in high-growth sectors such as artificial intelligence, climate technology, space technology, fintech infrastructure, and digital healthcare. Many are expected to play a significant role in shaping India’s next generation of innovation.

Successful Startup Founders in India

Many of India’s leading startups are built by founders who identified large market opportunities and executed consistently over long periods.

Some of the most influential startup founders in India include:

-

Nithin Kamath (Zerodha)

-

Falguni Nayar (Nykaa)

-

Kunal Shah (CRED)

-

Harshil Mathur (Razorpay)

-

Aadit Palicha (Zepto)

-

Peyush Bansal (Lenskart)

-

Bhavish Aggarwal (Ola)

-

Lalit Keshre (Groww)

These founders are frequently studied by entrepreneurs because of their ability to scale businesses, attract investment, and create long-term enterprise value.

FAQs – Frequently Asked Questions

1.Which startup is number 1 in India?

There is no single number one startup in India. Companies such as Zerodha, Razorpay, CRED, Groww, Nykaa, and Zepto are considered among the most successful startups based on revenue, market leadership, innovation, and customer adoption.

2. What are the top 10 startups in India?

Some of the top startups in India include CRED, Groww, Zerodha, Razorpay, Zepto, Nykaa, Meesho, Udaan, Lenskart, and Dream11.

3. Which startup sectors are growing fastest in India?

Artificial intelligence, fintech, SaaS, healthtech, climate technology, electric vehicles, and quick commerce are among the fastest-growing startup sectors in India.

4. Which city is known as the startup capital of India?

Bangalore is widely considered the startup capital of India because it hosts thousands of startups, venture capital firms, accelerators, and technology companies.

5. How do Indian startups raise funding?

Indian startups typically raise capital through angel investors, venture capital firms, family offices, strategic investors, government schemes, and private equity funds.

6. What makes a startup successful?

Successful startups usually combine strong product-market fit, scalable business models, effective customer acquisition, financial discipline, and strong leadership teams.

Raising Capital for Your Startup?

The startups featured in this guide did not grow through funding alone. They combined strong execution with the right capital strategy.

If you’re preparing for a seed round, Series A, growth capital raise, acquisition, or strategic partnership, FundTQ helps founders with:

✓ Investor readiness assessment

✓ Startup valuation

✓ Financial modelling

✓ Pitch deck preparation

✓ Investor outreach strategy

✓ Fundraising and M&A advisory

Speak with the FundTQ team to understand the most suitable funding path for your business stage.

Summary

What these startups have in common isn’t just scale — it’s intentionality. They raised smart, built defensible businesses, and treated capital as a tool rather than a goal. The startups above didn’t get there by accident. Behind almost every successful raise or exit is a team that understood the capital markets, ran a tight process, and walked into investor conversations fully prepared.

——————————————-

If you’re a founder thinking about your next equity raise, acquisition, or strategic exit — FundTQ’s advisory team has structured 200+ transactions across consumer, healthcare, and industrial sectors.

Talk to our team about what the right process looks like for your business.

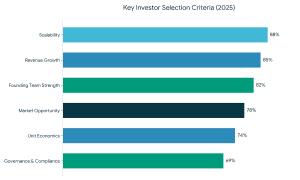

Post-ZIRP reality check:

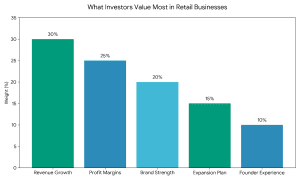

Post-ZIRP reality check: The brands in the closing round today have three characteristics in common: a brand story that can be defended, a healthy repeat customer, and a founder who can discuss their numbers fluently. In that case, capital is at your disposal.

The brands in the closing round today have three characteristics in common: a brand story that can be defended, a healthy repeat customer, and a founder who can discuss their numbers fluently. In that case, capital is at your disposal.

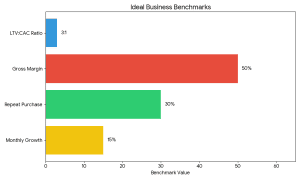

2. Customer Lifetime Value (LTV)

2. Customer Lifetime Value (LTV)

4. Gross Margin

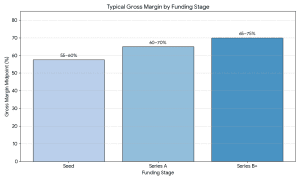

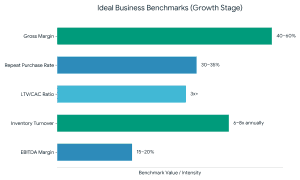

4. Gross Margin The automatic pass of most institutional investors is below 50% gross margin. It is no longer possible to have the room to finance acquisition, overhead and profitability at the same time.

The automatic pass of most institutional investors is below 50% gross margin. It is no longer possible to have the room to finance acquisition, overhead and profitability at the same time.

The following is a comprehensive guide on how to raise capital on an eCommerce business, which entails the sources of funds, the expectation of investors, strategies of valuation, and steps that can be taken to raise capital effectively.

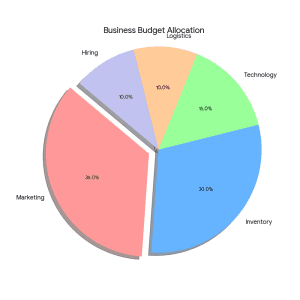

The following is a comprehensive guide on how to raise capital on an eCommerce business, which entails the sources of funds, the expectation of investors, strategies of valuation, and steps that can be taken to raise capital effectively. 1. Inventory Procurement

1. Inventory Procurement Understanding the

Understanding the  As someone involved in

As someone involved in

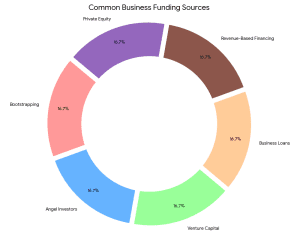

2. Startup Fundraising Advisory

2. Startup Fundraising Advisory 4. Investor-Ready Pitch Deck Strategy

4. Investor-Ready Pitch Deck Strategy Each sector demands specialized financial structuring, risk assessment, and investor mapping.

Each sector demands specialized financial structuring, risk assessment, and investor mapping.

It will not be any ordinary Investment Banking Firm in Mumbai that will simply raise capital, but will instead place your business in a position to achieve long-term enterprise value creation.

It will not be any ordinary Investment Banking Firm in Mumbai that will simply raise capital, but will instead place your business in a position to achieve long-term enterprise value creation.

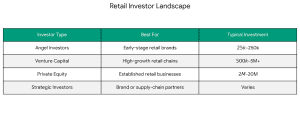

Early Stage (Pre-seed / Seed)

Early Stage (Pre-seed / Seed)

Building Your EdTech Pitch Deck: The 10 Essential Slides Investors Demand

Building Your EdTech Pitch Deck: The 10 Essential Slides Investors Demand

Even the most effective startup fundraising will not work without a powerful grip on these numbers.

Even the most effective startup fundraising will not work without a powerful grip on these numbers.

Technology startups have a higher initial expense than traditional businesses because of:

Technology startups have a higher initial expense than traditional businesses because of: AI Insight: The new AI can assist the founders to find out potential investors, fund raise trends, and even pitch deck optimization to predict what will attract investors according to previous funding records.

AI Insight: The new AI can assist the founders to find out potential investors, fund raise trends, and even pitch deck optimization to predict what will attract investors according to previous funding records.

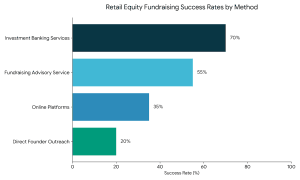

#5 Step: Leverage Networks and Platforms

#5 Step: Leverage Networks and Platforms