What Is Business Valuation And What Are Its Approaches?

Embarking on the intricate process of business valuation requires a nuanced understanding of diverse approaches and considerations. As the final steps unfold, the application of valuation methods and thoughtful adjustments becomes paramount. From assessing assets through the lens of the asset approach to projecting future benefits with the income approach and comparing with market trends via the market approach, each step contributes to unraveling the intricate tapestry of a company’s worth. Join us as we delve into the art and science of business valuation, decoding its complexities and shedding light on the crucial factors that shape a business’s ultimate value.

What is Business Valuation?

Business valuation is a critical process that provides a comprehensive understanding of a company’s worth. The final steps in this intricate journey involve the application of various approaches and the consideration of discounts that ultimately shape the conclusive value of a business interest. However, the proverbial “garbage in, garbage out” cautionary adage is vital in this context, emphasizing the significance of reliable financial information for an accurate valuation.

Business Valuation Approaches

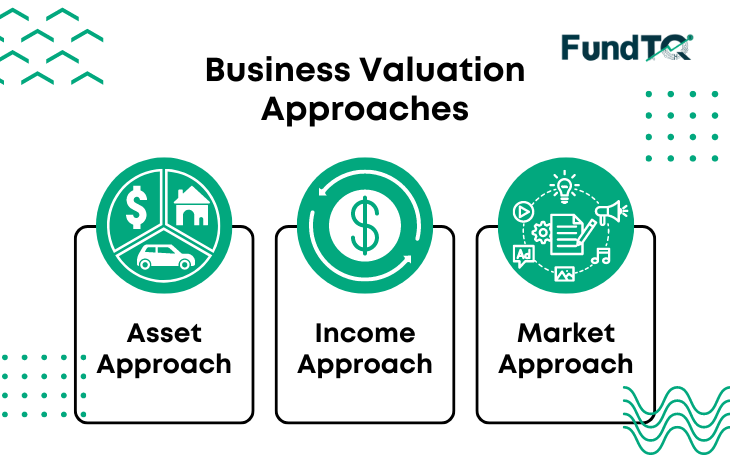

Three Pillars of Business Valuation: Asset, Income, and Market Approaches

1. Asset Approach

The asset-based approach, also known as the cost or replacement cost approach, calculates a company’s value by subtracting liabilities from the current value of all assets. Two common methods under this approach include the Adjusted Net Asset Method and the Capitalization of Excess Earnings Method. The former establishes a “floor value” by adjusting assets to fair market values, while the latter is a hybrid method blending asset and income approaches.

2. Income Approach

The income approach is often the primary method for operating companies. Key methods include the Capitalization of Cash Flow (CCF) Method and the Discounted Cash Flow (DCF) Method. The CCF method is a single-period model converting a company’s benefit stream into value, while the DCF method is a multiple-period model based on projecting future benefits and discounting them to present value.

3. Market Approach

The market approach allows for comparison with similar companies. Methods within this approach include the Guideline Transaction Method, Guideline Public Company Method, and Prior Transactions Method. These methods rely on transaction multiples derived from comparable sales, either private or public, to determine a company’s value.

Check out our business valuation software

Ownership Interest: Control and Marketability

The nature of the ownership interest being valued plays a crucial role in the final steps of business valuation. Understanding control and marketability is essential:

Control

– Controlling ownership (greater than 50%)

– 50%/50% ownership

– Minority interest (less than 50%)

Discounts for lack of control may be applied to non-controlling interests, ensuring a fair reflection of the power to influence company decisions.

Marketability

– Publicly traded (high liquidity)

– Privately held (low liquidity)

Discounts for lack of marketability may be necessary for privately held companies due to the complexities, costs, and time associated with selling ownership interests.

Conclusion

In summary, a successful business valuation involves understanding the purpose, standard of value, level of value, and the specific ownership interest in question. Collaboration with a valuation professional is crucial to selecting the most appropriate approaches and methodologies. Careful consideration of the company’s history, industry, economic outlook, and normalizing adjustments is key. Finally, recognizing the impact of ownership interest characteristics, such as control and marketability, ensures a nuanced and accurate business valuation.

Embark on the journey of business valuation armed with knowledge and a strategic approach to unlock the true worth of your enterprise.

Also Read: Purpose of Business Valuation