By a Senior Investment Banking Professional | 8+ Years in Venture Capital & Growth Financing

Bottom Line Up Front: Capital is available for D2C beauty brands in 2026–2027 — but only for founders who demonstrate financial discipline, authentic differentiation, and unit economics that actually work. This guide cuts through the noise and tells you exactly what investors want to see, what metrics matter, and how to raise successfully at every stage.

The State of D2C Beauty Funding Right Now

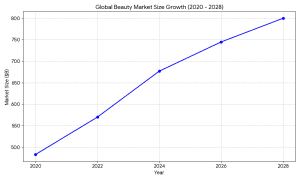

The beauty and personal care market in the world is projected to reach 800 billion dollars by 2028. Therein, direct-to-consumer beauty is among the most vigorously financed consumer verticals but the regulations have changed since the 20192022 funding craze.

Post-ZIRP reality check:

Post-ZIRP reality check:

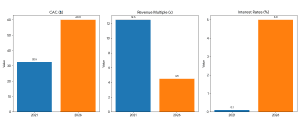

- CAC on Meta and Google doubled or tripled following iOS 14.5 privacy alterations.

- Interest rates had risen to 5%+, making inventory financing costly.

- Investors abandoned growth-at-all costs to unit economics discipline.

- Compression of revenue multiples – the 10x-15x ARR values of 2021 have disappeared.

The brands in the closing round today have three characteristics in common: a brand story that can be defended, a healthy repeat customer, and a founder who can discuss their numbers fluently. In that case, capital is at your disposal.

The brands in the closing round today have three characteristics in common: a brand story that can be defended, a healthy repeat customer, and a founder who can discuss their numbers fluently. In that case, capital is at your disposal.

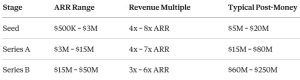

Funding Stages: What’s Expected at Each Level

The honest truth about seed in 2026: It is hard to find pre-revenue beauty brands that raise institutional seed capital. Investors desire 6-12 months of sales information that portrays that actual customers purchase, re-buy and refer. A beautiful brand with no customers would be more fundable than even 300K in revenue with a 35 percent 60-day repurchase rate.

The 5 Metrics That Make or Break Your Fundraise

1. Customer Acquisition Cost (CAC)

Formula: Total Sales & Marketing Spend ÷ New Customers Acquired

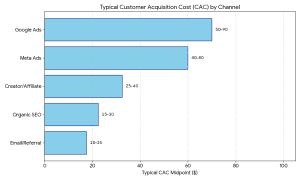

The defensible CAC of a product with a 4080 AOV is CAC3080 in case of beauty brands on Meta/Google in 2026. Above $100 CAC on sub-$50 AOV? That’s a structural red flag. The highest-ranking brands also exhibit a decreasing blended CAC with organic channels (creator affiliate, email, referral, SEO) increasing in the size of the acquisition.

2. Customer Lifetime Value (LTV)

2. Customer Lifetime Value (LTV)

Formula: AOV × Purchase Frequency × Customer Lifespan × Gross Margin

Don’t show projected LTV. Display real cohort data – how customers who got 6,12 and 18 months ago are really performing. Investors do not put much trust in modeled LTV; cohort evidence is what gets deals to get done.

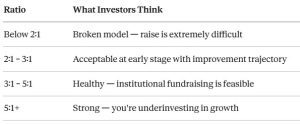

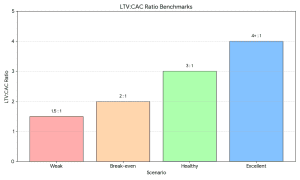

3. LTV:CAC Ratio — The North Star

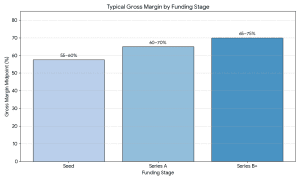

4. Gross Margin

4. Gross Margin

Beauty brands should target:

- Seed stage: 55–60%

- Series A: 60–70%

- Series B+: 65–75%

The automatic pass of most institutional investors is below 50% gross margin. It is no longer possible to have the room to finance acquisition, overhead and profitability at the same time.

The automatic pass of most institutional investors is below 50% gross margin. It is no longer possible to have the room to finance acquisition, overhead and profitability at the same time.

5. Contribution Margin

Formula: Revenue – COGS – Variable Marketing – Variable Fulfillment

This is the most honest signal of economic health. A brand can show 65% gross margin but negative contribution margin if CAC and fulfillment are excessive. Series A investors in 2026 expect contribution margin positivity — ideally 15–25% per order.

What Investors Actually Evaluate: The 4-Pillar Framework

Pillar 1: Brand Differentiation

The most widespread investor pass of all: “Why should this brand exist, and why can we have it in 18 months at Sephora as the house brand? What forms a genuine moat: proprietary formulation, clinical efficacy information, the genuine founder-to-consumer relationship, and an owned (email, SMS, subscription) rather than rented (Instagram followers) community.

Pillar 2: Unit Economics Health

Covered above. The brief one: you cannot march through your CAC, LTV, gross margin, and contribution margin without memorizing it, cohort data to support it, then you are not prepared to have an institutional conversation.

Pillar 3: Team and Operational Capability

Beauty is an operations company. Brands that have been developed through marketing are killed by supply chain failures, stockouts and 3PL disasters. Investors seek founders which have real CPG or beauty operating experience, or a team that fulfill those gaps in a credible way.

Pillar 4: Market Size and Exit Optionality

No VC would be investing in a brand that is a peak of 15M in revenue. Investors are underwriting a journey to strategic purchase (L’Oréal, Unilever, Shiseido, Estee Lauder, P&G) or category leadership at scale. The question your pitch should respond to is: Who will be buying this brand, and at what price, in 5-7 years?

Funding Sources: Matching Capital to Your Stage

1. Angel Investors and Pre-Seed

The most outstanding beauty angels are former beauty executives, CPG operators, and founders that have already left. They come with capital and distribution relationship, introduction of retail and formulation credibility.

Location: Cosmoprof North America, CEW events, BeautyMatter NEXT, AngelList syndicates, warm LinkedIn introductions with current portfolio founders.

2. Seed VCs Active in Beauty

At seed, Forerunner Ventures, CircleUp Growth Partners, XRC Labs, and consumer-themed micro-funds are the most active. The trick here is to reach investors with a current portfolio consisting of brands adjacent to yours – evidence that they have a thesis consistent with yours.

3. Series A/B Funds

The active Series A/B investors in beauty and personal care include Prelude Growth Partners, Alliance Consumer Growth, Stripes Group, General Catalyst (consumer), and New Enterprise Associates.

4. Strategic Corporate Investors

Various conglomerates have venture arms, which invest and open doors:

- Unilever Ventures personal care and wellness, seed to growth.

- L’Oréal BOLD – disruptive brand innovation and beauty technology.

- Shiseido Ventures (SBVC) – skincare startup and beauty innovation.

- LVMH Luxury Ventures – high and luxury beauty positioning.

A major warning: Strategic investment with L’Oréal could dilute your alternatives with other acquirers such as Estée Lauder or Unilever. Know the strategic implications prior to signing.

Also Read: Startup Funding in India: A Complete Guide

5. Non-Dilutive Alternatives Worth Knowing

Revenue-Based Financing (RBF): Clearco, Wayflyer, Pipe, and Capchase are offering $100K-5M at a percentage of monthly revenue. Ideally applicable to inventory financing and performance marketing scale-up not general working capital. APR must be effective greater than 60; it should only be deployed in high-ROI, short-payback applications.

Purchase Order Financing: PO financing is offered to brands launching in Sephora, Ulta or Target with a substantial initial PO so that you can fund production along a confirmed purchase order and still the equity is not diluted. One of the most important tools beauty founders realize when it is too late.

Valuation Reality Check: 2026–2027 Benchmarks

Valuation premium drivers: Subscription revenue of above 30% of mix, gross margin of above 65, proprietary formulation or IP, founder exit history, and omnichannel presence have significant multiple premiums.

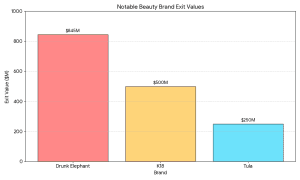

Contextual exits Similar exits in the recent past:

- K18 → Unilever (2023): $500M+ -disciplined unit economics, scale quickly.

- Tula → Procter & Gamble (2022): ~$250M+

- Drunk Elephant→ Shiseido (2019):~845M, 10x revenue.

It is these that the investors are simulating when they consider your brand.

The Fundraising Playbook: 3 Things That Separate Closers from Pitchers

1. Prepare for 90 Days Before Your First Investor Conversation

People who put in the effort to close rounds fast are founders who are planning to raise money like a product launch, and not improvisation.

- Recalculate P&L with contribution margin visibility.

- Create tables of cohort analysis (by month of acquisition, 6/12/18 months out)

- Calculate CAC channel by channel rather than blended.

- Prepare a 24-month cash flow base/bull/bear.

- Diligence Prepare genuine responses to the 10 most difficult questions.

2. Target Investors With Thesis Precision

The quickest way to 60 rejections and a de-motivated founder is a spray-and-pray approach to reaching out to investors. Each outreach should respond: Does this fund have a consumer thesis? Have they made previous investments in beauty? Is the amount and level of my stage and check size appropriate to their fund? Half the number of targeted warm-introduction outreaches will beat 200 cold emails every time.

3. Create Competitive Dynamics — Don’t Negotiate in a Vacuum

Investors act when they are in a hurry. Organize a process with a set-out date. Get several investors interested at the same time, not in different stages. Be open concerning competitive interest. The commitment by a lead investor promotes all the subsequent conversations between co-investors.

5 Fundraising Mistakes That Kill Beauty Rounds

- Starting investor conversations before your data is ready. First impressions in venture are durable. Wait until your traction is undeniable.

- Raising at 2021-era valuations. Investors know the comps. Overpriced rounds stall or die.

- 90%+ paid acquisition dependency. If your entire growth engine is Meta/Google, one algorithm change ends the business. Investors model this risk heavily.

- No cohort analysis. Asking for a Series A without cohort data is like asking for a mortgage without a credit score.

- Underestimating the timeline. Seed rounds take 3–6 months. Series A takes 4–9 months. Founders running on 60 days of runway negotiate from desperation — and investors know it.

Quick-Reference FAQ

Q. How much should I raise at seed?

1.5M to 5M, in size to allow you 18-24 months to achieve Series A-ready performance (5M-10M ARR, 3:1+ LTV:CAC, 60-percent gross margin).

Q. Do I need retail before raising a Series A?

No – but a signed retail term sheet makes the story count in a real sense. Retail growth that is unplanned and places stress on working capital is a warning as opposed to a qualification.

Q. What gross margin do I need for institutional investors?

55% to be in conversation; 60% needs to be taken seriously at Series A.

Q. How do investors evaluate a beauty brand’s moat?

There are four dimensions, which include: formulation defensibility, brand equity depth (owned community, not rented followers), distribution advantage, and founder authenticity.

Q. Should I use a placement agent for my raise?

In the case of seed and Series A, run it yourself with strong advisors. Placement agents impose some real value on Series B+ ($25M+) where process complexity warrants the fee of 3-5%.

The Bottom Line

D2C beauty is among the most attractive consumer investment categories in 2026-2027 – the fundraising environment rewards preparation, financial fluent, and genuine differentiation. Investors will find capital founders who have a command of their unit economics as well as brand narrative, who create owned communities and not rented audiences and who come to investors with conviction supported by data.

The ones who do not will realize that a beautiful brand and an excellent founder story is no longer sufficient.