FCFF vs FCFE is one of the most important concepts in corporate finance and business valuation. Investors, founders, private equity firms, and investment bankers use these cash flow metrics to determine what a business is worth and make informed investment decisions. While both metrics measure a company’s ability to generate cash, they serve different valuation purposes. Understanding the difference between Free Cash Flow to Firm (FCFF) and Free Cash Flow to Equity (FCFE) is essential when building DCF models, raising capital, evaluating acquisitions, or assessing shareholder value.

What is the Difference Between FCFF and FCFE?

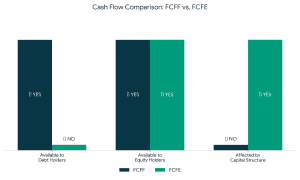

The key difference between FCFF and FCFE is that FCFF measures cash available to all capital providers, including debt and equity investors, while FCFE measures cash available only to equity shareholders after debt obligations are met.

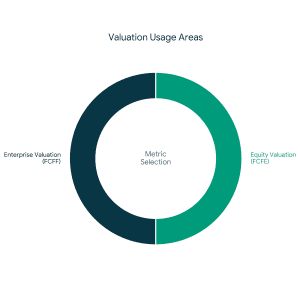

FCFF is commonly used to calculate enterprise value, whereas FCFE is used to estimate equity value.

FCFF vs FCFE: Formulas, Definitions, and Calculation Methods

Let’s first build a basic knowledge of each statistic before exploring the differences between FCFF vs FCFE.

Let’s first build a basic knowledge of each statistic before exploring the differences between FCFF vs FCFE.

Free Cash Flow to Firm (FCFF):

FCFF is the amount of cash generated by a company that is available to all capital providers, including debt and equity investors, after taxes, operating expenses, and capital expenditures.

It functions as an indicator of the cash flow that is accessible to all investors, irrespective of the capital structure of the business. This formula is used to calculate FCFF:

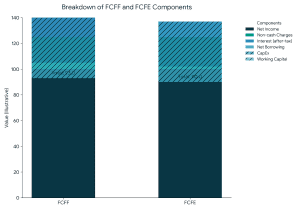

FCFF = Net Income + Non-cash Charges + Interest (1 – Tax Rate) – Capital Expenditures – Changes in Working Capital

Free Cash Flow to Equity (FCFE):

In contrast, FCFE represents the cash available to equity shareholders after accounting for all expenses, reinvestment needs, and debt obligations. It shows the amount of cash flow that can be given to equity investors without endangering the business’s viability as a whole. This formula is used to calculate FCFE:

FCFE = Net Income – (Capital Expenditures – Depreciation) – Changes in Working Capital + Net Borrowing

Knowing the formula is only the first step. In practice, valuation professionals rarely rely on formulas alone. The accuracy of an FCFF or FCFE valuation depends heavily on assumptions regarding growth rates, debt levels, capital expenditure requirements, and future cash flow projections.

Key Differences Between FCFF and FCFE:

While both FCFF and FCFE provide insights into a company’s cash flow dynamics, they differ significantly in their scope and applicability. Here are the key distinctions between the two metrics:

While both FCFF and FCFE provide insights into a company’s cash flow dynamics, they differ significantly in their scope and applicability. Here are the key distinctions between the two metrics:

| Parameter | FCFF | FCFE |

|---|---|---|

| Represents | Cash available to all capital providers | Cash available to equity shareholders |

| Valuation Output | Enterprise Value | Equity Value |

| Discount Rate | WACC | Cost of Equity |

| Debt Impact | Excluded | Included |

| Preferred For | M&A and DCF valuation | Equity valuation |

FCFF vs FCFE: When Should You Use Each?

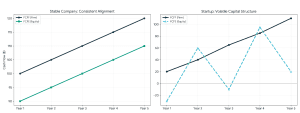

Use FCFF when valuing the entire business, performing DCF valuation, analyzing acquisition opportunities, or evaluating companies with changing debt structures. Use FCFE when estimating shareholder returns, valuing equity directly, or analyzing mature companies with stable leverage.

1. Perspective:

FCFF represents the cash flow that is accessible to all capital sources, including holders of debt and equity. The cash flow that is available to equity stockholders once debt obligations are taken into account is the primary focus of FCFE.

2. Capital Structure:

Changes in the company’s capital structure have no effect on FCFF because it takes into account cash flows that are accessible to all capital providers. FCFE considers the capital structure of the business as well as how debt financing affects the cash flows of equity shareholders.

3. Reinvestment Assumptions:

Only the cash flows available to equity owners for reinvestment or distribution are taken into account by FCFE; all other cash flows, including those attributable to debt holders, are assumed to be reinvested back into the company.

4. Valuation Implications:

To ascertain the inherent worth of a business’s activities, discounted cash flow (DCF) valuation models frequently employ the FCFF method. In equity valuation models, FCFE is used to calculate the fair value of a company’s common share.

During fundraising, mergers, acquisitions, and strategic investments, choosing between FCFF and FCFE can materially affect valuation outcomes. Professional investors often prefer FCFF because it evaluates the entire enterprise before considering financing decisions.

Founder Insight: Many startups use FCFF-based valuation models during fundraising because debt structures, reinvestment requirements, and ownership dilution can change significantly across funding rounds. Before approaching investors, founders should understand how valuation assumptions affect ownership dilution and fundraising outcomes.

Try FundTQ’s Free Business Valuation Tool to estimate your company’s value before your next fundraising discussion.

Practical Applications of FCFF vs FCFE:

For a variety of financial studies and decision-making procedures, it is essential to comprehend the subtle differences between FCFF and FCFE. The following are some real-world uses for both metrics:

From our experience advising on 200+ fundraising, M&A, and strategic transactions, including assignments led by professionals from IIT Delhi, KPMG, PwC, and EY backgrounds, cash flow methodology selection often has a significant impact on valuation conclusions.

1. Investment Valuation:

– FCFF is employed in DCF models to assess the intrinsic value of a company’s operations, considering all capital providers’ perspectives.

– FCFE, which focuses on the cash flows to equity owners, is used in equity valuation models to determine the fair value of a company’s stock.

From our experience advising on 200+ fundraising, M&A, and strategic transactions, we have found that valuation outcomes are often driven more by cash flow assumptions and capital structure decisions than by the valuation model itself. This is particularly relevant in acquisition transactions where buyers evaluate enterprise value rather than only shareholder value.

2. Capital Budgeting:

– Analysts use FCFF to assess whether investment projects can generate value for all capital providers.

– FCFE assists in evaluating investment projects’ viability from the standpoint of equity shareholders, taking shareholder wealth into account. Furthermore, it offers valuable insights into the potential returns and risks associated with such projects.

3. Financial Planning and Analysis:

– FCFF aids in assessing a company’s financial performance. It also helps determine its ability to generate cash flows to meet debt obligations and fund future growth.

– FCFE assists in evaluating the company’s capacity to distribute dividends, repurchase shares, or undertake other actions to enhance shareholder value. Moreover, it provides valuable insights into the company’s financial health and its potential for long-term growth.

When Should Businesses Use Professional Valuation Support?

While FCFF and FCFE provide useful frameworks for understanding business value, real-world transactions require deeper analysis. Fundraising, M&A transactions, ESOP issuance, shareholder exits, and strategic investments often involve assumptions around growth rates, discount rates, debt structures, and comparable market benchmarks.

In these situations, a professionally prepared valuation can provide greater confidence for founders, investors, and acquirers when making financial decisions.

Conclusion:

FCFF and FCFE are both powerful valuation tools, but they answer different questions. FCFF focuses on cash flows available to all capital providers and is widely used in enterprise valuation, while FCFE focuses on cash available to equity shareholders. For startups, growth-stage businesses, and acquisition transactions, FCFF is often preferred because it remains less affected by changing capital structures. Understanding when to use each methodology can significantly improve valuation accuracy and investment decision-making.

Whether you’re preparing for fundraising, evaluating an acquisition, issuing ESOPs, or assessing shareholder value, selecting the right valuation framework is critical. FundTQ has advised on 200+ transactions across fundraising, M&A, and strategic advisory engagements. If you’re looking for a transaction-ready valuation, connect with our team for an expert review of your business.

Also Read– Startup Due Diligence

FCFF vs FCFE FAQ:

Q1: Which cash flow metric do investment bankers use most often?

A: Investment bankers generally prefer FCFF because it values the entire enterprise and remains less affected by capital structure changes. This makes FCFF particularly useful in mergers, acquisitions, and fundraising transactions.

Q2: Is FCFF or FCFE more accurate?

A: Neither is inherently more accurate. FCFF and FCFE answer different valuation questions. FCFF is generally preferred when valuing the entire business, while FCFE is more suitable when focusing exclusively on equity value.

Q3: Why is FCFF preferred over FCFE in M&A transactions?

A: FCFF is generally preferred in mergers and acquisitions because buyers acquire the entire business, not just its equity. It therefore provides a more comprehensive measure of enterprise value.

Q4: Which is better for startup valuation: FCFF or FCFE?

A: FCFF is typically preferred for startup valuation because startups often have evolving capital structures, changing debt levels, and significant reinvestment requirements.

Q5: Can two analysts using FCFF arrive at different valuations?

A: Yes. Differences in growth assumptions, discount rates, working capital forecasts, and capital expenditure projections can lead to significantly different valuation outcomes.

Comment (01)